Download Colorado Dr 1317 Form in PDF

Common mistakes

-

Failing to provide the correct organization name. The name must match the official registration of the donee organization.

-

Not including the license number or Colorado account number. This information is essential for proper identification.

-

Leaving out the FEIN (Federal Employer Identification Number). This is necessary for tax processing.

-

Providing an incorrect address or failing to include the city, state, and zip code. Accurate information is crucial for correspondence.

-

Not filling in the donor's full name correctly. Both the last and first names must be included.

-

Overlooking the Social Security Number or Colorado account number. This is required for the donor’s identification.

-

Miscalculating the donation amounts. Ensure the qualifying donation is accurately derived from the donation amount minus any non-qualifying donations.

-

Not signing the form. The preparer’s signature is necessary for validation.

-

Failing to retain a copy of the completed form for record-keeping. Both the donor and donee organization should keep copies.

-

Not submitting the form with the Colorado income tax return. This form must accompany the tax return to claim the child care contribution credit.

Documents used along the form

The Colorado DR 1317 form is essential for claiming the Child Care Contribution Tax Credit. However, it is often accompanied by various other forms and documents that facilitate the donation process and ensure compliance with state regulations. Below is a list of related documents frequently used alongside the DR 1317 form.

- Form DR 1778: This form is used to claim the Child Care Contribution Tax Credit on a Colorado income tax return. Donors must include this form when submitting their tax filings.

- Form DR 0104: This is the Colorado Individual Income Tax Return form. It is necessary for all Colorado residents to report their income and claim various credits, including the Child Care Contribution Tax Credit.

- Form DR 1098: This form serves as a record of charitable contributions made by the donor. It provides documentation needed for tax purposes and is often required by the IRS.

- Form 990: Nonprofit organizations must file this form annually to provide financial information to the IRS. It helps ensure transparency and accountability in how donations are utilized.

- Form W-9: This form is used to request the taxpayer identification number of the donor. It is often completed by the donor and submitted to the donee organization for record-keeping purposes.

- Donation Receipt: A written acknowledgment from the donee organization that details the donation amount and the purpose of the contribution. This receipt is important for the donor’s tax records.

- California Horse Bill of Sale: To ensure a smooth transfer of ownership, utilize the California Templates for proper documentation.

- Allocation Letter: This document outlines how the donated funds will be allocated within the organization. It is particularly useful for donors who wish to specify how their contributions are used.

- Organizational By-Laws: These documents outline the governance structure and operational procedures of the donee organization. They provide insight into how the organization functions and how donations are managed.

Understanding these forms and documents is crucial for both donors and donee organizations. Proper completion and submission of these materials ensure compliance with Colorado tax laws and facilitate the claiming of tax credits effectively.

Understanding Colorado Dr 1317

-

What is the Colorado DR 1317 form?

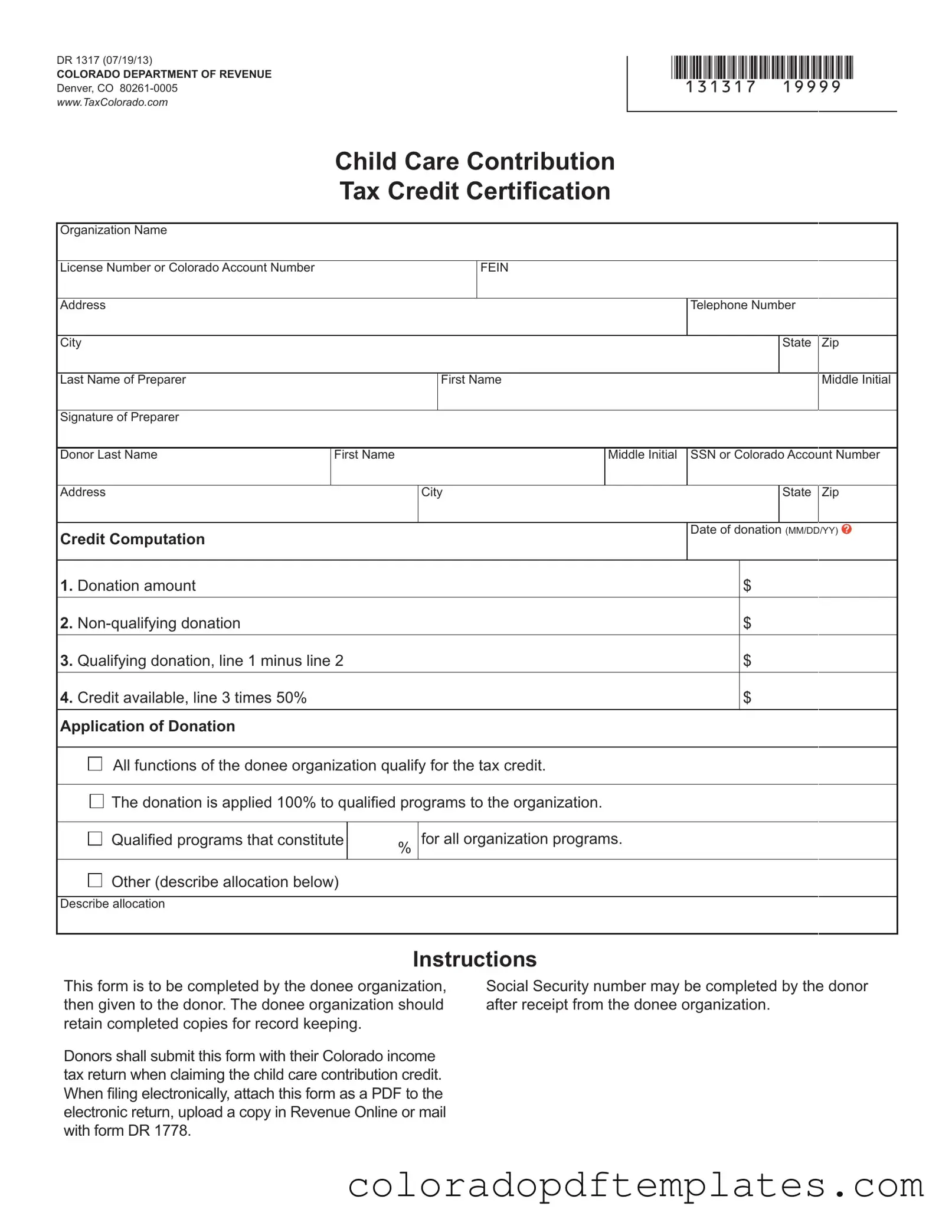

The Colorado DR 1317 form is a certification used for claiming the Child Care Contribution Tax Credit. It is completed by the organization that receives donations for child care programs. This form helps donors receive a tax credit for their contributions.

-

Who needs to fill out the DR 1317 form?

The donee organization must complete the DR 1317 form. This organization is responsible for providing the form to donors after they make a contribution. Donors will use this form when filing their Colorado income tax returns.

-

What information is required on the form?

The form requires several details, including:

- Organization name

- License number or Colorado account number

- Federal Employer Identification Number (FEIN)

- Address and contact information

- Donor's name and Social Security Number or Colorado account number

- Donation amount and details regarding qualifying and non-qualifying donations

-

How does a donor calculate the tax credit?

To calculate the tax credit, the donor needs to follow these steps:

- Determine the total donation amount.

- Identify any non-qualifying donations.

- Subtract non-qualifying donations from the total to find the qualifying donation.

- Multiply the qualifying donation by 50% to find the credit available.

-

What should donors do with the completed form?

Once the form is completed by the donee organization, donors should keep it for their records. They must submit this form with their Colorado income tax return to claim the Child Care Contribution Tax Credit.

-

Can the DR 1317 form be submitted electronically?

Yes, donors can submit the form electronically. When filing online, they should attach the completed DR 1317 form as a PDF. Alternatively, they can upload a copy in Revenue Online or mail it with form DR 1778.

-

What happens if a donor’s Social Security number is not provided?

If the donor’s Social Security number is not provided on the form, they can fill it in after receiving the completed form from the donee organization. It is important for the donor to include this information when filing their tax return.

-

How long should organizations keep copies of the DR 1317 form?

The donee organization should retain completed copies of the DR 1317 form for their records. Keeping these records is essential for proper documentation and to support the claims made by donors on their tax returns.

-

Are there any specific programs that qualify for the tax credit?

Yes, the donation must be applied to qualified programs within the organization to qualify for the tax credit. The form allows organizations to describe how the donation is allocated among their programs.

-

Where can I find more information about the DR 1317 form?

For more details, you can visit the Colorado Department of Revenue's website at www.taxcolorado.com. This site provides resources and additional information regarding tax credits and related forms.

Browse Other Templates

Getting a Colorado License - Providing thorough details can strengthen a victim's case against identity theft.

For those navigating the complexities of vehicle ownership, understanding the importance of a streamlined process is vital. A reliable resource for this is the New York Motor Vehicle Power of Attorney template, which provides clarity and efficiency in managing your vehicle transactions.

How to Get Tabor Refund 2024 - For additional assistance, resources are available to clarify any uncertainties regarding the estimated tax penalty process.

Misconceptions

Misconceptions about the Colorado DR 1317 form can lead to confusion for both donors and organizations involved in the child care contribution tax credit process. Understanding the realities of this form is essential for proper compliance and maximizing benefits. Below are six common misconceptions.

- The DR 1317 form is only for large donations. Many believe that only substantial contributions qualify for the tax credit. In reality, any donation made to a qualified organization can be eligible, regardless of the amount.

- Only specific organizations can issue the DR 1317 form. Some individuals think that only certain types of organizations, such as large nonprofits, can provide this form. However, any qualified child care organization recognized by the state can issue the DR 1317.

- The form must be submitted with the donation. A common misunderstanding is that the DR 1317 form must accompany the donation at the time it is made. Instead, the form is completed by the donee organization and given to the donor after the donation is made.

- Donors must complete the form themselves. Some donors believe they are responsible for filling out the DR 1317 form. In fact, the donee organization is responsible for completing the form, ensuring all necessary information is accurately provided.

- The credit is automatically applied. Many assume that simply making a donation guarantees the tax credit will be applied. Donors must actively submit the completed DR 1317 form with their income tax return to claim the credit.

- All donations qualify for the full credit amount. It is a misconception that every donation qualifies for the full 50% credit. Donors must be aware that only qualifying donations, after deducting any non-qualifying amounts, will be eligible for the credit.

Understanding these misconceptions can empower donors and organizations to navigate the process more effectively, ensuring that contributions to child care programs are maximized for tax benefits.