Download Dr 1083 Colorado Form in PDF

Common mistakes

-

Failing to provide complete names and addresses for all transferors. Each transferor's last name, first name, middle initial, and address must be accurately listed.

-

Not checking the correct box for the type of transferor. Ensure that the appropriate category (individual, estate, corporation, trust, etc.) is selected.

-

Omitting Social Security Numbers (SSNs) or Colorado Account Numbers. These identifiers are crucial for processing the form.

-

Incorrectly stating the type of property sold. Specify whether the property is residential, commercial, or another type.

-

Misreporting the selling price of the property. This amount must reflect the total contract sales price, including any liabilities assumed.

-

Not checking the box if Colorado tax was withheld. If applicable, this box must be marked to indicate withholding.

-

Failing to provide a reason for not withholding tax when applicable. Select the appropriate affirmation to explain why withholding did not occur.

-

Neglecting to sign the form. Both transferors and any applicable spouses must sign to validate the document.

-

Submitting the form after the deadline. The form must be filed within 30 days of the closing date to avoid penalties.

Documents used along the form

The DR 1083 form is essential for reporting the conveyance of real property interests in Colorado. When completing this form, several other documents may also be required or helpful. Below is a list of commonly used forms and documents that complement the DR 1083.

- DR 1079: This form is used to report the amount of Colorado tax withheld during the sale of real property. It must be filed with the DR 1083 if withholding occurs.

- Form 1099-S: This federal form reports the sale of real estate to the IRS. It provides essential details about the transaction and is often referenced in conjunction with the DR 1083.

- Affidavit of Title: This document certifies the seller’s ownership of the property and confirms that there are no undisclosed liens or claims against it. It helps protect the buyer’s interests.

- Closing Disclosure: This form outlines the final terms of the mortgage loan, including all costs associated with the transaction. It ensures transparency between the buyer and seller regarding financial obligations.

- Horse Bill of Sale: This form is essential for transferring ownership of a horse in California. It includes important details about the horse and the transaction, ensuring a smooth transfer. For additional information and a template, visit California Templates.

- Deed: The deed is the legal document that transfers ownership of the property from the seller to the buyer. It must be recorded in the county where the property is located.

- Title Insurance Policy: This document protects against any defects in the title that were not discovered during the closing process. It provides peace of mind to the buyer regarding their ownership rights.

- Property Disclosure Statement: This statement provides information about the property's condition and any known issues. Sellers are often required to disclose material defects to potential buyers.

- Sales Contract: This legal agreement between the buyer and seller outlines the terms of the sale, including the purchase price and any contingencies that must be met.

- IRS Form 8288: This form is used by foreign persons to report and pay tax on the sale of U.S. real property interests. It may be necessary for non-resident sellers.

- Local Transfer Tax Forms: Some municipalities impose transfer taxes on property sales. These forms are required to report and pay any applicable local taxes.

Understanding these documents can help streamline the process of selling or buying real estate in Colorado. Proper preparation ensures compliance with state and federal regulations, protecting all parties involved in the transaction.

Understanding Dr 1083 Colorado

What is the DR 1083 form used for?

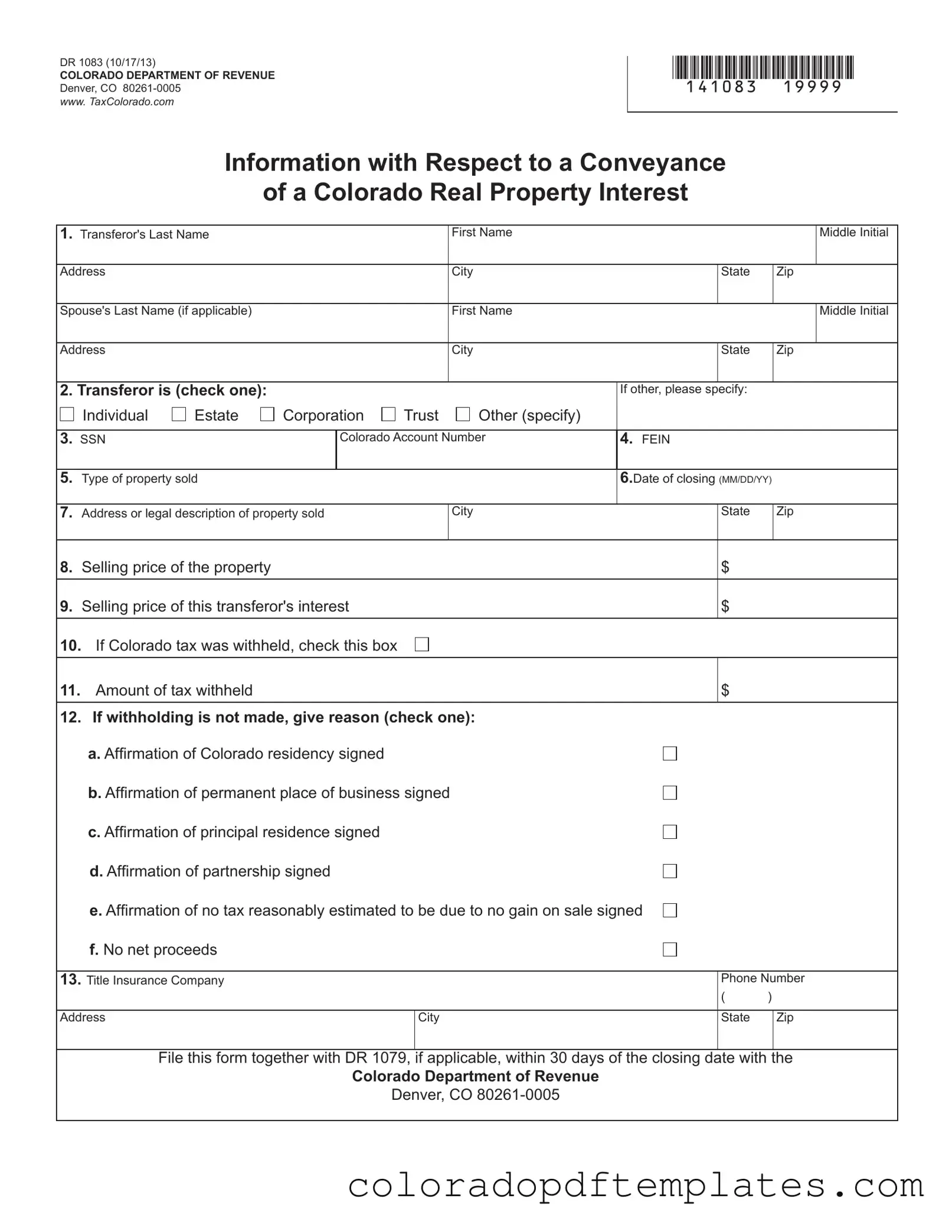

The DR 1083 form is utilized to report the conveyance of a real property interest in Colorado. It is specifically designed for situations where Colorado tax may be withheld from the proceeds of a property sale. This form must be filed with the Colorado Department of Revenue within 30 days of the closing date if tax was withheld or if it would have been withheld but for certain affirmations made by the transferor.

Who needs to fill out the DR 1083 form?

Any transferor involved in the sale of Colorado real property valued at $100,000 or more may need to complete the DR 1083 form. This includes individuals, estates, corporations, and trusts. If there are multiple transferors, each must submit a separate form unless they are married and choose to be treated as a single transferor.

What information is required on the DR 1083 form?

The form requires various details, including:

- The names and addresses of the transferor and, if applicable, the spouse.

- The type of entity transferring the property (individual, corporation, etc.).

- Social Security Number or Colorado Account Number.

- The type of property sold and its legal description.

- The selling price of the property and the transferor's interest.

- Details about any tax withheld.

- Information about the title insurance company involved in the transaction.

What are the withholding tax requirements?

Generally, sales of Colorado real property valued at $100,000 or more by non-residents are subject to withholding tax. The withholding is typically 2% of the selling price or the net proceeds, whichever is less. However, there are exceptions where withholding is not required, such as when the transferor has a Colorado address or if the selling price is below the threshold.

What happens if tax is withheld?

If Colorado tax is withheld, the title insurance company or closing agent must complete the DR 1079 form to transmit the withheld tax to the Colorado Department of Revenue along with the DR 1083. This process must occur within 30 days of the closing date to avoid penalties.

What if tax is not withheld?

If tax is not withheld, the transferor must provide a reason by checking the appropriate box on the form. Possible reasons include affirmations of residency, a permanent place of business, or that no tax is reasonably estimated to be due. Each affirmation must be signed under penalty of perjury.

What are the penalties for not filing the DR 1083 form?

If the title insurance company or closing agent fails to file the DR 1083 form when required, they may face penalties. The penalty can be either $500 or 10% of the amount that should have been withheld, with a maximum penalty of $2,500. Timely filing is essential to avoid these financial consequences.

Where can I find more information about the DR 1083 form?

Additional information and resources regarding the DR 1083 form can be found on the Colorado Department of Revenue's website at www.taxcolorado.com. For specific inquiries, individuals can also contact the department at (303) 238-SERV (7378).

Browse Other Templates

Division of Real Estate Colorado - The agreement includes specific obligations for both the seller and buyer during the occupancy period.

Colorado Bonded Title - The Colorado DR 2394 form is designed for those needing to establish vehicle title via a surety bond.

For those needing assistance with motor vehicle transactions, the efficient Motor Vehicle Power of Attorney form empowers vehicle owners to authorize a trusted individual to manage essential vehicle-related activities on their behalf.

Colorado Wage Withholding Account - In addition to a sales tax license, businesses can apply for a wholesale license using this form.

Misconceptions

Understanding the DR 1083 form in Colorado can be challenging. Here are some common misconceptions that people often have about this important document:

- Misconception 1: The DR 1083 form is only for individuals.

- Misconception 2: If I am a Colorado resident, I don't need to file the DR 1083.

- Misconception 3: The form is only necessary for properties sold over $100,000.

- Misconception 4: Only the seller needs to complete the DR 1083.

- Misconception 5: I can submit the DR 1083 anytime after the closing.

- Misconception 6: If no tax is withheld, I don't need to file the DR 1083.

- Misconception 7: The DR 1083 is the only form I need to worry about.

- Misconception 8: I can estimate the selling price for the form.

- Misconception 9: All properties sold in Colorado are subject to withholding tax.

This form is applicable to various types of transferors, including corporations, estates, and trusts. It's not limited to individuals.

Even Colorado residents must file the form if Colorado tax was withheld or if they are claiming an exemption.

The threshold for withholding tax is indeed $100,000, but the form may still be required for lower sales if certain conditions apply.

While the seller typically fills out the form, the title insurance company or closing agent also plays a crucial role in submitting it.

The form must be filed within 30 days of the closing date. Missing this deadline can lead to penalties.

This is not true. The form is required even if tax is not withheld, especially if an exemption is claimed.

In many cases, the DR 1079 must also be submitted if tax is withheld, making it essential to check both forms.

The selling price should reflect the actual contract sales price and not an estimated figure.

There are exceptions, such as when the property is sold for less than $100,000 or if the transferor meets specific criteria.

Being informed about these misconceptions can help ensure compliance and avoid unnecessary complications when dealing with real estate transactions in Colorado.